Oil Prices Leave Uneven Impact on Offshore Sector

Given the slide in oil price over the last six months, it is not a surprise to see companies in the petroleum industry reducing costs, whether it be capital expenditure (capex) or operating expenditure (opex). But not all firms felt the full impact of lower oil price simultaneously – those operating in the development segment are mostly continuing business as usual, while those involved in exploration have been hit by cutbacks in operations, speakers told the Singapore Offshore Finance Forum earlier this month.

The shift towards a lower oil price environment commenced in the second half of 2014 when benchmark Brent oil futures fell below the psychologically significant $100 a barrel in early September. The decline in Brent prices mirrored the earlier fall in U.S. West Texas Intermediate oil futures which broke through the $100 a barrel mark in late July.

The decision by the Organization of Petroleum Exporting Countries (OPEC) to not cut oil production last November had exacerbated the problem of abundant supplies in the markets, resulting in further downward pressure on oil prices.

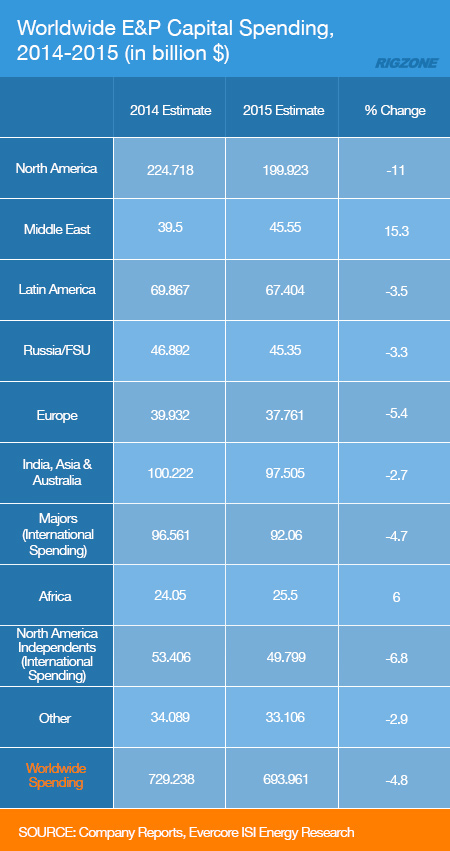

Hurt by falling revenue, many oil producers, including international oil companies (IOC) and national oil companies (NOC), have reduced their capex and opex, which have in turn impacted the rest of the petroleum industry.

“This is a period of uncertainty. Companies are not sure at this point what will happen going forward, projects are being pared back this year, next year and certainly until things get back into a natural equilibrium ... expensive projects such as U.S. shale, oil sands, some of the ultra deepwater, the Arctic … will be delayed until oil price gets up to the right level,” Jason Waldie, an associate director of Douglas-Westwood Pte. Ltd., told forum participants in Singapore.

The absence of any clarity on the direction of oil price adds further to the uncertainty for seeking project approvals in the near term as the low price environment is forecast to last between one and three years, speakers at the forum commented.

“Our view [on oil price] is … around $60 a barrel this year … [and it] might be stabilizing there for 2016 … The most expensive oil will not be developed in the current time. Oil companies don’t want to take FID [final investment decision],” ABN AMRO’s Senior Energy Banker Jan-Hein Jesse said.

Uneven Impact on Offshore Sector

Seismic firms are among the first to be adversely affected by spending cutbacks in the oil and gas industry as they stand at the forefront of the exploration and development cycle, making them an easier target for cost reduction than others that are further down the development process.

Norway’s Petroleum Geo-Services was one of those hit by low oil prices. It revealed Feb. 12 that its first quarter 2015 earnings will be weak as “low oil price and cautious spending behaviour among oil companies continue to impact bidding, pricing and vessel utilization. Visibility is low and we are continuing our proactive approach to prepare for the challenging year ahead.”

ABN AMRO’s Jesse agreed that business for seismic companies had been hurt in recent months as they are the first to be contracted for potential projects, but he believed that the impact on these companies have already bottomed out.

“For the drillers, we haven’t seen the trough yet. We still believe … dayrates will go down further and we haven’t seen the worse yet. For floating production contractors, they are slightly behind but they haven’t seen the worse either,” he added.

Likewise, Jesse felt that the SURF (subsea umbilicals, risers and flowlines) segment has not been affected by the current low oil price environment as they have enough backlog in orders. However, 2016 would be quite difficult for companies operating in this segment.

In fact, subsea firms with a huge backlog in their supply chain (Subsea 7 S.A., Aker Solutions, Technip S.A., etc.) may need “a couple of years to get their backlog down … so I am not surprised that they are not too unhappy about that,” Waldie said.

Similarly for installation companies like The Netherlands-based Heerema and big crane vessel companies, “they will have a fantastic year in 2015 because they are fully booked, but 2016 is already slower and for 2017 they don’t see the projects and they have difficulty in filling the backlog,” Jesse explained.

Yards Less Exposed

Meanwhile, Singapore’s Triyards Holding Ltd., an integrated engineering, fabrication and ship construction solutions provider which operates mainly out of its yards in Vung Tau and Ho Chi Minh City in Vietnam, has not been impacted directly by the current downtrend in oil price.

“From a yard perspective, we will a little bit less exposed to a prolonged situation [of low oil price]. We have the flexibility of moving to other asset classes, whether they are self-elevated units, lift boats, offshore support vessels, anchor handlers,” company CEO Chan Eng Yew said at the forum.

WHAT DO YOU THINK?

Generated by readers, the comments included herein do not reflect the views and opinions of Rigzone. All comments are subject to editorial review. Off-topic, inappropriate or insulting comments will be removed.

- Malaysia's InvestKL Woos Top Oil, Gas MNCs to Base in Kuala Lumpur

- Petrobangla Invites EOIs for 3 Offshore Exploration Blocks in Bay of Bengal

- Malaysia's SapuraKencana Posts 7.1% Gain in 2Q FY17 PAT to $27M

- TH Heavy Engineering, McDermott End Partnership in Malaysia

- Singapore's NUS Slowly Builds its Petroleum Engineering Program

- What's Next for Oil? Analysts Weigh In After Iran's Attack

- Venezuela Authorities Arrest Two Senior Energy Officials

- CNOOC Bags Contract for 4.6 MMcf of LNG for Philippines

- EU Gas Storage Nearly 60 Percent Full at End of Heating Season

- EIA Raises WTI Oil Price Forecasts

- ExxonMobil Makes FID on 6th Project in Contested Guyana Asset

- Is The Iran Nuclear Deal Revival Project Dead?

- ORE Catapult Looks for New CEO as Jamieson Steps Down

- Japan's Mizuho Invests $3.64MM in Bison's CCS Project in Alberta

- Equinor Advances First Battery Storage Projects in USA

- Macquarie Strategists Warn of Large Oil Price Correction

- JPMorgan CEO Says LNG Projects Delayed Mainly for Political Reasons

- USA, Venezuela Secretly Meet in Mexico as Oil Sanctions Deadline Nears

- EIA Ups Brent Oil Price Forecast for 2024 and 2025

- Petrobras Discovers Oil in Potiguar Basin

- EIR Says Oil Demand Will Not Peak Before 2030

- Biden Plans Sweeping Effort to Block Arctic Oil Drilling

- Pantheon Upgrades Kodiak Estimates to 1.2 Billion Barrels

- Dryad Flags Red Sea 'Electronic Warfare' Alert

- Russian Oil Is Once Again Trading Far Above the G-7 Price Cap Everywhere

- Oil and Gas Executives Predict WTI Oil Price

- New China Climate Chief Says Fossil Fuels Must Keep a Role

- Chinese Mega Company Makes Another Major Oilfield Discovery

- Oil and Gas Execs Reveal Where They See Henry Hub Price Heading

- Equinor Makes Discovery in North Sea

- ExxonMobil Racks Up Discoveries in Guyana Block Eyed by Chevron

- Macquarie Strategists Warn of Large Oil Price Correction

- DOI Announces Proposal for Second GOM Offshore Wind Auction

- Standard Chartered Reiterates $94 Brent Call

- Chevron, Hess Confident Embattled Merger Will Close Mid-2024