Rig Trends: Gulf of Mexico Jackup Market Showing Effects of Slowdown

The collapse in the price of oil has begun to take its toll on Gulf of Mexico jackup utilization and dayrates. Since June 2014, oil prices have fallen by 57 percent and could go even lower. In a region where the number of marketed rigs has fallen to just 32 units, cold-stacking has begun and will likely increase during the remainder of the year. Operators are slashing 2015 spending plans and rig owners are doing the same with dayrates in an attempt to keep as many rigs working as possible. The following will summarize the current market as well as look at what can be expected for the rest of 2015.

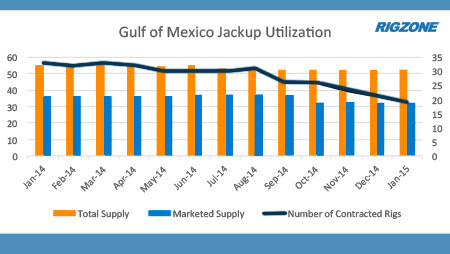

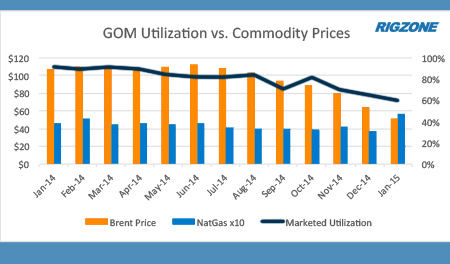

As of mid-January 2015, there were 49 jackups in the Gulf of Mexico. Total supply in the region has fallen dramatically in the past several years, as has the marketed fleet, which are those rigs reported by contractors to be actively marketed for work. Typically, it is the marketed supply number that is most often used when discussing utilization in any area, and that is what this article will use as well. As of mid-January 2015, there were 32 marketed jackups in the Gulf. Only 19 of those are currently under contract for utilization of just 59.4 percent. To provide some historical context, one would have to go back to September 2009 to find that few jackups under contract in the Gulf. Figure 1 shows monthly Gulf of Mexico jackup total and marketed supply along with utilization since January 2014. One year ago, marketed utilization stood at 91.7 percent with 33 of 36 rigs under contract. During the same period, the price for Brent crude fell from an average of $107 in January 2014 to $50 a year later. Historically, jackup utilization has been compared to natural gas prices as the two tracked virtually the same, but that ceased in early 2009 when gas prices fell sharply. When that occurred, Gulf operators focused primarily on their oil plays as that price was well over $100 per barrel. Figure 2 plots monthly Gulf of Mexico marketed jackup utilization along with Brent oil prices and Henry Hub natural gas prices since January 2014. The utilization increase in October 2014 was not due to an increase in contracted rigs, but rather a number of marketed jackups that were cold-stacked which resulted in a temporary utilization increase.

Within the fleet, certain segments are faring better than others. As is normally the case, the premium jackup fleet, that is independent-leg, cantilever jackups with a rated water depth of 250 feet or more, is doing the best. Currently, 14 of the 18 marketed units in this segment are under contract for utilization of 78 percent. That leaves utilization for the remainder of the fleet at just 36 percent, with only five of 14 rigs under contract. Obviously, any rig can be cold stacked at any time, but based on these numbers, it is likely that any additional rigs removed from the marketed fleet will come from the latter category.

So, what about dayrates? For contract fixtures, there are many variables to consider when looking at the numbers and sometimes timing is everything. For most of 2014, rig owners were able to either maintain prior rates or realize very small increases in most of their new contracts or renewals. The first sign of trouble occurred in September when a 300’-IC contract extension was inked at $110,000, a $20,000 drop from its prior rate. It then took until November for rates as a whole to begin falling. Based on data from RigLogix, for all of 2014 there were just 52 jackup fixtures meaning the total number of new deals signed in any one month is not large and not every segment of the fleet has a new fixture every month. However, comparisons for a few key jackup classes can be made. In January 2014, the average new fixture rate for ultra-premium jackup (350’-IC and greater rated) rates was $155,000. In December, the average was $105,625, a 32 percent drop. For 300’-IC units, leading edge rates have suffered a similar fate, dropping from an average of $130,000 in early 2014 to around $100,000 in January 2015, a 30 percent fall.

Clearly, the question on everyone’s mind is what is going to happen the rest of 2015 and beyond. First and foremost, the price of oil is one of the major drivers for rig demand worldwide and where it ultimately settles is anyone’s guess. Oil prices are determined by energy demand, and those pundits who study that are not predicting a demand increase in the near term. Nevertheless, many economists and energy analysts believe oil prices could rebound by the end of this year, with some predicting that prices will ultimately settle in the $70-$75 range. Of course, wars or other geo-political events can change everything in an instant, so what ends up occurring is anyone’s guess. Regardless of outside influences, however, until there is improvement beyond current oil and natural gas prices, rig utilization and dayrates worldwide will continue to fall.

In regards to Gulf of Mexico jackup utilization and dayrates, it is clear that the market is in for a fairly prolonged rough patch. In 2015, utilization will fall under 50 percent as rig owners will not be able to cold stack their way to higher numbers. It should follow that the premium and ultra-premium fleets will continue to enjoy the highest utilization as they are most in demand at the moment. However, some contractors have in selected instances already bid their largest jackups below $100,000/day, so the only question is how low will rates go? We previously mentioned the 30 percent drop in rates for a couple of fleet segments, but there clearly is room for further reductions. In down markets the rate gap between jackup classes always narrows and this time will be no exception. The range of the most recent fixtures for the entire fleet is $77,500 to $117,500. We expect the range could ultimately fall somewhere in the $50,000-$80,000 range, but when that happens is likely several months away.

WHAT DO YOU THINK?

Generated by readers, the comments included herein do not reflect the views and opinions of Rigzone. All comments are subject to editorial review. Off-topic, inappropriate or insulting comments will be removed.

- Rig Trends: Offshore Rig Fleet Poised for Comeback, but More Time is Needed

- Rig Trends: Offshore Rig Market Recovery Reports Premature

- Rig Trends: 2017 Offshore Rig Market Not in for Much Improvement

- Niger Delta Leaders Want Army Out And Oil Firms To Relocate To Region

- No Near-Term Recovery For Offshore Rig Market

- An Already Bad Situation in the Red Sea Just Got Worse

- USA Regional Banks Dramatically Step Up Loans to Oil and Gas

- Oil Markets Were Already Positioned for Iran Attack

- Valeura Makes Three Oil Discoveries Offshore Thailand

- North America Breaks Rig Loss Streak

- EU Offers $900MM in Funding for Energy Infrastructure Projects

- Germany to Provide $2.3B Aid for Decarbonization of Industrial Sectors

- Mexico Presidential Frontrunner Plans to Spend Billions on RE, Gas Power

- Chile's ENAP Says Working on Decarbonization Plan

- House Votes to Sanction China's Purchase of Iranian Oil

- Macquarie Strategists Warn of Large Oil Price Correction

- JPMorgan CEO Says LNG Projects Delayed Mainly for Political Reasons

- USA, Venezuela Secretly Meet in Mexico as Oil Sanctions Deadline Nears

- EIA Ups Brent Oil Price Forecast for 2024 and 2025

- Petrobras Discovers Oil in Potiguar Basin

- EIR Says Oil Demand Will Not Peak Before 2030

- Biden Plans Sweeping Effort to Block Arctic Oil Drilling

- Pantheon Upgrades Kodiak Estimates to 1.2 Billion Barrels

- Dryad Flags Red Sea 'Electronic Warfare' Alert

- USA Crude Oil Stocks Rise Almost 6MM Barrels WoW

- Oil and Gas Executives Predict WTI Oil Price

- New China Climate Chief Says Fossil Fuels Must Keep a Role

- Chinese Mega Company Makes Another Major Oilfield Discovery

- Oil and Gas Execs Reveal Where They See Henry Hub Price Heading

- Equinor Makes Discovery in North Sea

- ExxonMobil Racks Up Discoveries in Guyana Block Eyed by Chevron

- Macquarie Strategists Warn of Large Oil Price Correction

- DOI Announces Proposal for Second GOM Offshore Wind Auction

- Standard Chartered Reiterates $94 Brent Call

- Chevron, Hess Confident Embattled Merger Will Close Mid-2024