Musings: Are We Entering The Capitulation Phase of Industry Cycle?

This opinion piece presents the opinions of the author.

It does not necessarily reflect the views of Rigzone.

Oil price action during the past two weeks may be signaling that we are entering the “capitulation phase” of the oil industry cycle. If so, news and angst within the business will grow worse as despair and panic will come to dominate the outlook. Surprisingly, this may be a good thing. The challenge is that the level of despair and destruction must rise much higher than we are currently witnessing. But various data points suggest we may be seeing the first shifts in industry mindsets that will lead to substantive actions that will cause industry’s fundamentals to change. While some readers might think we are crazy to suggest that events are setting the stage for the industry’s recovery, we would point out that our concept of a recovery may not match what others consider a recovery – but that’s a discussion for another Musings.

A quick review of the industry cycle to date will set the stage for the balance of our discussion. Crude oil prices peaked in June 2014 and slowly slid down as we transitioned from mid-summer to late fall that year. During the fall of last year, the industry’s focus was on the growing surplus of global oil output with most of the attention directed to the rapid growth in U.S. liquids supply due to the success of the shale revolution. The drilling rig count continued to grow after the June oil price peak. It rose almost up to the shock of OPEC’s decision in late November, led by Saudi Arabia, to allow market forces to determine global crude oil prices, which changed the industry’s future. As crude oil prices fell from over $100 a barrel in mid-June 2014 to the $80s a barrel in November, the Baker Hughes (BHI-NYSE) active drilling rig count rose from roughly 1,850 rigs (1,540 oil and 310 gas rigs) to 1920 rigs (1,575 oil and 345 gas), or a nearly 4% increase.

After that fateful OPE meeting and Saudi Arabia’s declaration that it would continue to produce at its highest level ever and allow oil prices to find a market-clearing price. The Kingdom’s announcement signaled it was shifting its oil strategy from defending high prices to reclaiming the market share it had lost by following its prior policy of defending high oil prices. For most of November prior to the OPEC meeting on Thanksgiving Day, the media chronicled the travels of OPEC oil ministers going from meeting to meeting involving both OPEC members and non-OPEC producers seeking to orchestrate a coordinated global oil production cut. That hope was dashed with Saudi Arabia’s announcement.

What most industry participants and analysts understood was that OPEC’s decision would dramatically alter the industry’s future. The consensus assumption that oil prices would stay in the $80-$100 a barrel range was no longer operable – profitability would be under significant assault. The questions everyone sought answers to were: How quickly would oil prices fall? How low would they fall? How much oilfield activity would be lost? What would happen to E&P economics and the financial health of the service industry? Management teams went into over-drive through the end of 2014 revising their 2015 business plans and future strategies based on their assessment of answers to the above questions.

As E&P and oilfield service companies reported their year-end earnings, management teams began addressing their revised business plans. The actions required to adjust business plans were dictated by management’s view of the length and depth for this industry downcycle. Super-imposed on those business plan adjustments were considerations dictated by the state of company balance sheets, which often forced more unpleasant decisions.

As oilfield activity collapsed, service companies were the first to move by slashing field workforces and home office support personnel. Some cuts appeared drastic while others seemed more moderate. The magnitude of the reductions reflected either the optimistic or pessimistic view management teams held of their future. Analysts, industry management teams and investment professionals debated the answer to the length and depth question by picking a letter of the alphabet that would best mirror the shape of the decline and recovery of oil prices. The choices – “V”, “U”, “W” and “L” – are based on examining past drilling rig cycles and trying to match the current industry cycle against them.

With the recent completion of the second quarter earnings reporting season, combined with July’s dramatic oil price decline – the worst monthly drop since the 2008 financial crisis - and last week’s fight to hold oil prices above $40 a barrel, despair over the outlook has engulfed the industry. Multiple forecasters have cut their oil price projections for 2015, but importantly they have cut them for 2016, which signals they believe tough times for the oil patch will continue until 2017. These oil price forecast cuts coincided with energy company announcements of additional capital spending reductions, layoffs of more employees and consultants and other steps to preserve balance sheet strength by cutting dividends, stopping or severely reducing stock buybacks, and selling assets to reduce debt. Those companies most financially levered and suffering significant declines in revenues have been forced to seek bankruptcy protection. That assumes they could not restructure their debt to allow the company to continue to operate without significant debt relief. The blood-letting is now beginning!

One ingredient in this downcycle not as evident in past cycles is the role of capital – both public and private. As we have written about in the past, the energy business has raised substantial capital in the first half of 2015. According to the Financial Post, Canadian publicly-traded E&P companies raised C$10.5 (US$8.0) billion in 2015’s first half, up from C$8.2 (US$6.2) billion in 2014’s second half, but down from the C$11.4 (US$8.6) billion raised in the first half of 2014. In the U.S., news service Bloomberg reported that E&P companies have raised over $1 billion per month in new equity for the first six months of 2015, but in July, as the oil price was collapsing, the industry could only raise $300 million of new equity. During the first half of 2015, the E&P industry sold $6 billion in assets and the outlook is for increased sales volumes through the end of year. The Bloomberg article quoted John Walker, the CEO of EnerVest Ltd., a Houston-based investment firm that specializes in buying and operating orphaned assets, as saying that he believed there could be as much as $20 billion in E&P asset sales before the end of the year. All of these capital-raising activities are supplemented by the billions of dollars of private equity capital available that is targeting energy investments.

The only piece of good news in the above recap of capital flows into the energy sector is that in July, the industry could only raise a fraction of what its average monthly take had been during the prior six months. We know investment bankers are suggesting to management teams that the window for energy companies to tap capital markets is now essentially closed. The bankers hope the capital window may re-open following Labor Day, but that judgement was made prior to the oil price and stock market falls of last week.

Private equity funds continue to prowl the energy sector seeking attractive investment opportunities. So far, they have been thwarted by the readily-available capital from public markets and the lack of agreement on the value of assets and/or companies being marketed. These valuations will change as investors gain greater confidence in the industry’s outlook, even if it is bad. Valuations may be changing as we write this article. That change is necessary as a first step in this phase of restructuring the industry.

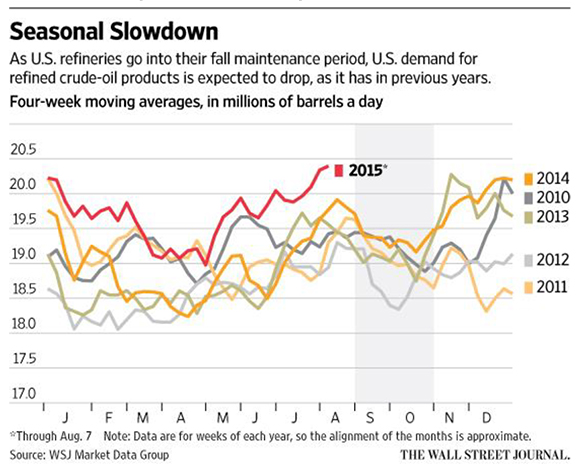

One of the greatest challenges for oil prices in the near term is the calendar. We are moving into that time of the year when North American energy demand weakens due to the end of the summer vacation season. That means driving slows and gasoline demand weakens. As a result, refiners shut down their plants to re-configure them to produce more heating oil and less gasoline as they prepare for the upcoming winter.

During September, crude oil demand weakens as shown in Exhibit 2. Low U.S. oil demand will put greater downward pressure on crude oil prices.

Lower crude oil and natural gas prices mean the E&P industry will have less revenue and less cash flow to reinvest in their business. The magnitude of the cash flow reduction also depends on companies’ finances, i.e., how much debt they have. The shock from the collapse of crude oil prices in recent weeks, merely a couple of months after they had rebounded from the low $40s a barrel to over $60 a barrel this spring, comes just as management teams are starting their 2016 budgeting process. This chaos also arrives just as commercial banks enter their borrowing-base redeterminations for their E&P company borrowers. This is a critical period for E&P companies as these redeterminations will provide a new assessment of the value of company assets and how much banks are willing or able to lend against them. To the extent E&P companies already have high debt loads, any reduction in their borrowing bases will force them to either raise additional capital or cut back their activities. Depending upon their options, they may even be forced to sell assets or possibly the company.

An additional factor impacting the E&P industry is the reduction in their portfolios of hedge contracts for their future oil production. For much of 2015, E&P companies have been living off past hedges that paid them maybe $80-$90 a barrel when the oil would have sold in the spot market for $50-$60 a barrel. The companies received an extra $30 a barrel in revenue and cash flow, which enabled some management teams to avoid the difficult cost-cutting decisions. As crude oil prices have traded within a $45-$60 a barrel range for most of 2015, the ability of E&P companies to hedge at meaningful premiums to current spot prices has been limited. When crude oil prices rallied this spring, some producers hedged production at marginal premiums to their costs. On the other hand, some E&P management teams found that the hedge price did not provide them with much profit over their cost so they elected to gamble that the oil price recovery would continue. Since oil prices are now sharply lower, these producers are left accepting spot oil prices, which will limit their ability to conduct activity in the future.

These conditions are pressuring the E&P industry and will force companies to confront difficult choices – cut activity/spending more, seek financial relief in some manner, or elect to leave the industry. No choice is attractive. All of them entail pain – both emotional and financial. This is part of the blood-letting that must occur before the industry can correct itself. But we are actually seeing some tough decisions being made. About 20 oil sands expansion projects in Canada have been delayed. Consultant Wood Mackenzie says over 200 industry projects have been postponed, limiting future oil output. The latest offshore lease sale was the weakest since 1986.

Last week was the 20th annual EnerCom oil and gas conference. EnerCom is an energy company communications consultant that helps many with their investor relations efforts. When we were on Wall Street, we attended this conference, which is unique in that it welcomes both buyside and sellside energy investment professionals. One sellside E&P analyst attended the conference and provided comments about the presentations. His Day One report stated that EnerCom reported that their registration for the conference was 7% higher than in 2014. The firm also reported that companies had very high numbers of one-on-one investor meetings scheduled. The analyst reported that he mostly saw familiar faces in the audience, which supports the investment bankers’ views that the public market window for energy companies to raise capital is now virtually non-existent. The industry will need “new” investors to successfully raise large amounts of new capital.

This analyst made a couple of other interesting observations. He said he questioned E&P management teams about their view of the level for oil prices that would generate returns similar to those earned when crude oil was at $90 a barrel and finding and development costs were much higher than today’s. In his view, the consensus was that $60-$70 a barrel is the “new $90 a barrel” oil given lower well costs and improved corporate efficiencies. He also said that producers acknowledged that returns were “skinny” with crude oil in the low $40s a barrel. We aren’t sure what “skinny” equates to, but we suspect not much profit, if any at all.

We were interested in his other observation, which dealt with how producers are coping with the current environment. He said that producers seemed to be reverting to the “1980’s playbook.” What does that mean? How about drilling within cash flow and attempting to hold production flat. What novel concepts! What someone who didn’t live through the ‘80’s and ‘90’s might not understand is that the playbook resulted from there not being cheap capital and private equity money available then. In fact, following the demise of Continental Illinois Bank in Chicago and Penn Square Bank in Oklahoma City, commercial banks almost outlawed energy lending in the 1980’s as it was considered too speculative, so there was virtually no new capital available. Today, we live in a world driven by easy money policies globally, meaning zero interest rates, which contributed to the high oil prices of 2009-2014 and the surge in capital flowing into private equity funds. A recent quote from economist and money manager Gary Shilling highlights this phenomenon and its damage to the energy industry. He said:

“The oil optimists noted that earlier high oil prices, aided by low financing costs, had pushed up production, especially among U.S. frackers. Low prices, they reasoned, would curb production, especially since fracked wells tend to be short-lived and the cost of drilling new ones exceeded the depressed prices. But a funny thing happened on the way to $80 oil: The rally stopped dead in its tracks at about $60 in May and June, then slid to the current $42, a new low.

“Me? I'm sticking with my forecast of $10 to $20 a barrel.”

Why does Mr. Shilling predict such a low oil price? His prediction rests on the economic principle that commodity prices are usually set by the marginal cost of production, which he believes is in the $10-$20 a barrel range for locations such as the Permian basin and the Middle East, among a few other conventional oil producing regions. In effect, Mr. Shilling is pointing to the underlying mechanics behind the commodity “super-cycle” that some people believe ended a few years ago. That view says we are firmly in the down part of the commodity cycle but that it will eventually return us to higher commodity prices but probably not for five or more years.

The concept underlying the super-cycle is that the boom in global demand for raw materials in response to high growth and the build-out of developing economies, especially China, caused an explosion in basic commodity prices. Those high prices were necessary to drive producers to expand their capacity, which was made easier by zero interest rates following the 2008 financial crisis. As the era of cheap capital continued, it drove commodity output and capacity growth, but economic weakness caused a collapse in demand that was magnified by the amount that commodity prices such as basic materials declined as producers were striving to make any profit or generate positive cash flow by selling their output. It was only as prices continued falling, reaching levels that inflicted significant damage on the financial health of these producers that production was shut down and new capacity additions deferred or stopped completely. Oil and gas seem to be the only commodities where producers have been reluctant to stop increasing their output. That would seem to be at odds with the sharp fall in the drilling rig count, but it may reflect the increased efficiencies within the E&P sector. What is unknown at the present time is whether the recent bump up in the drilling rig count reflects a delayed response to the higher oil prices seen in May and June, or the desperate actions of producers needing to generate any cash flow to try to survive this downturn.

A resumption in the decline in the drilling rig count would be a signal that producers were serious about ending their serial destruction of capital. Our sense is that we may see the rig count begin to decline again. It has already begun happening in Canada, which may signal that capital discipline is beginning to be embraced by producers up there. This would be another indication that we have entered into the capitulation phase of the industry cycle.

While we are laying out what may be taken as an optimistic industry outlook by suggesting we are entering the capitulation phase of the cycle, we would be negligent to not detail how the recovery might play out. In all honesty, we are not sure what the recovery’s timing will be or how dramatic it might be. Our head says we could see all the conditions for an improvement to be in place by the end of 2015, some five months from now. Unfortunately, our “gut” says the recovery may not start until 2017 or maybe even later. At this point, we are confident that we are in the bottom phase of the industry cycle. The question is whether this will be a bottom shaped like the letter “U” or rather like a bathtub as suggested by others. Although we are confident that people are changing their outlooks, we are not convinced enough minds have been changed yet for a quick recovery to commence. Any near-term “U-shaped” oil price recovery, in our judgment, would likely morph into a “W” pattern and extend the ultimate recovery. For the time being, we will reserve describing our view of how the recovery will unfold.

WHAT DO YOU THINK?

Generated by readers, the comments included herein do not reflect the views and opinions of Rigzone. All comments are subject to editorial review. Off-topic, inappropriate or insulting comments will be removed.

Managing Director, PPHB LP

- What's Next for Oil? Analysts Weigh In After Iran's Attack

- Venezuela Authorities Arrest Two Senior Energy Officials

- CNOOC Bags Contract for 4.6 MMcf of LNG for Philippines

- EU Gas Storage Nearly 60 Percent Full at End of Heating Season

- EIA Raises WTI Oil Price Forecasts

- ExxonMobil Makes FID on 6th Project in Contested Guyana Asset

- Is The Iran Nuclear Deal Revival Project Dead?

- ORE Catapult Looks for New CEO as Jamieson Steps Down

- Japan's Mizuho Invests $3.64MM in Bison's CCS Project in Alberta

- Equinor Advances First Battery Storage Projects in USA

- Macquarie Strategists Warn of Large Oil Price Correction

- JPMorgan CEO Says LNG Projects Delayed Mainly for Political Reasons

- USA, Venezuela Secretly Meet in Mexico as Oil Sanctions Deadline Nears

- EIA Ups Brent Oil Price Forecast for 2024 and 2025

- Petrobras Discovers Oil in Potiguar Basin

- EIR Says Oil Demand Will Not Peak Before 2030

- Biden Plans Sweeping Effort to Block Arctic Oil Drilling

- Pantheon Upgrades Kodiak Estimates to 1.2 Billion Barrels

- Dryad Flags Red Sea 'Electronic Warfare' Alert

- Russian Oil Is Once Again Trading Far Above the G-7 Price Cap Everywhere

- Oil and Gas Executives Predict WTI Oil Price

- New China Climate Chief Says Fossil Fuels Must Keep a Role

- Chinese Mega Company Makes Another Major Oilfield Discovery

- Oil and Gas Execs Reveal Where They See Henry Hub Price Heading

- Equinor Makes Discovery in North Sea

- ExxonMobil Racks Up Discoveries in Guyana Block Eyed by Chevron

- Macquarie Strategists Warn of Large Oil Price Correction

- DOI Announces Proposal for Second GOM Offshore Wind Auction

- Standard Chartered Reiterates $94 Brent Call

- Chevron, Hess Confident Embattled Merger Will Close Mid-2024