Oil and Gas M&A in 2Q 2013 Reaches Just $23.6B

This opinion piece presents the opinions of the author.

It does not necessarily reflect the views of Rigzone.

As we embark upon a new quarter, Evaluate Energy has taken the time to reflect on the key trends that emerged during the second quarter of 2013 in the oil & gas M&A market, including the impact of NOCs and the transition of substantial gas discoveries during 2012 into multi-billion dollar deals.

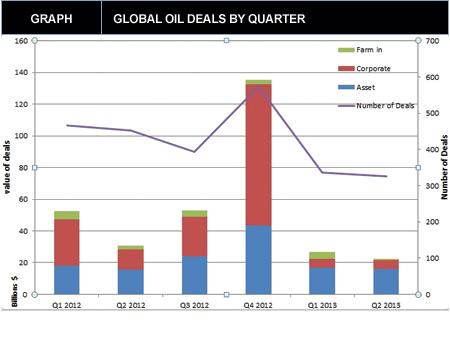

The most significant statistic to emerge from the data is that the total deal value in the upstream sector during Q2 2013 came to just $23.6 billion, lower than any other quarter since Q3 2009. Q3 2009 had its own strong reasons for being sluggish; during the quarter the credit crisis had claimed its first major victim with the collapse of Lehman Brothers, the US Henry Hub gas benchmark fell below $2 and oil prices were still recovering after plummeting to $30 at the end of 2008. The explanation behind the latest quarter’s lacklustre performance, however, lacks the same drama; oil and gas prices have shown stability during the quarter at $90 per barrel of oil and $4 per mcf of gas in the US. Economic uncertainty still lingers though especially within the austerity-hit European market and many CEOs are erring to the side of caution when it comes to expanding beyond their company’s reach.

Due to these reasons, perhaps it’s no surprise that the largest deals during the quarter involved national oil companies, who are less influenced by short and medium term economic fluctuations. The largest deal of the quarter involved ONGC and Oil India, who acquired a 10% stake in the 100+ tcf gas discovery offshore Mozambique in the Rovuma basin for $2.5 billion from Videocon Industries. The $0.50 cost per recoverable mcf of gas reserves would usually represent good value but commercialization of the asset is at least 5 years away and will require large upfront payments to develop the field and construct the necessary LNG exporting terminal which would have made this field fall short of many public company’s investment appraisals. The deal follows the acquisition of Cove Energy at the end of 2012 when another national oil company, PTT, keen to gain control of the company’s flagship asset of an 8.5% interest in the Rovuma Offshore Area 1, paid $2.2 billion.

The next largest deal involved Lukoil acquiring the Russian assets of Hess Corp for $2.05 billion. The deal was initially expected to raise little over $1 billion so the price negotiated can be seen as a coup for Hess. With Russia’s steep production and corporate taxes, typical per proven barrel of reserve metrics seldom exceed $5 per boe (Rosneft acquired TNK-BP for $5.13 per boe of proven reserves in 2012), yet the Hess deal equates to approximately $25 per proven boe for the oil rich assets.

Chinese companies were uncharacteristically quiet in terms of new deals during the quarter with only one notable transaction taking place; Sinopec acquired a 10% interest in Block 31 offshore Angola. In the past couple of years, Chinese-based companies averaged $8.4 billion of new global E&P deals per quarter, yet in Q2 2013, this deal between Sinopec and Marathon made the total just $1.5 billion. Despite the lack of traditional M&A, China did grab the world’s attention when it agreed a crude oil marketing deal with Rosneft worth $270 billion over 25 years to import 300,000 b/d including a $70 billion upfront cash payment.

The third largest deal also came from Africa with Petrobras divesting a 50% stake in all of its African operations for $1.525 billion to Banco BTG Pactual S.A.. The divestment is part of Petrobras’ $9.9 billion divestment plan to partly fund development of its huge pre-salt oil reserves off the coast of Brazil, which will require $107 billion investment over the next 5 years. The deal involves 73.9 million boe of proven reserves which are 95% oil and 57% developed, along with a considerable portfolio of exploration assets. Given the amount of exploration upside in the deal the price paid per proven reserve of $20.63 represents an impressive deal for the buyer.

12

View Full Article

WHAT DO YOU THINK?

Generated by readers, the comments included herein do not reflect the views and opinions of Rigzone. All comments are subject to editorial review. Off-topic, inappropriate or insulting comments will be removed.

- How Likely Is an All-Out War in the Middle East Involving the USA?

- Rooftop Solar Now 4th Largest Source of Electricity in Australia

- US Confirms Reimposition of Oil Sanctions against Venezuela

- Analyst Says USA Influence on Middle East Seems to be Fading

- EU, Industry Players Ink Charter to Meet Solar Energy Targets

- Russian Ships to Remain Banned from US Ports

- Brazil Court Reinstates Petrobras Chair to Divided Board

- EIB Lends $425.7 Million for Thuringia's Grid Upgrades

- Var Energi Confirms Oil Discovery in Ringhorne

- Seatrium, Shell Strengthen Floating Production Systems Collaboration

- An Already Bad Situation in the Red Sea Just Got Worse

- What's Next for Oil? Analysts Weigh In After Iran's Attack

- USA Regional Banks Dramatically Step Up Loans to Oil and Gas

- EIA Raises WTI Oil Price Forecasts

- How Likely Is an All-Out War in the Middle East Involving the USA?

- Venezuela Authorities Arrest Two Senior Energy Officials

- Namibia Expects FID on Potential Major Oil Discovery by Yearend

- Oil Markets Were Already Positioned for Iran Attack

- Is The Iran Nuclear Deal Revival Project Dead?

- Petrobras Chairman Suspended

- Oil and Gas Executives Predict WTI Oil Price

- An Already Bad Situation in the Red Sea Just Got Worse

- New China Climate Chief Says Fossil Fuels Must Keep a Role

- Oil and Gas Execs Reveal Where They See Henry Hub Price Heading

- Equinor Makes Discovery in North Sea

- Macquarie Strategists Warn of Large Oil Price Correction

- DOI Announces Proposal for Second GOM Offshore Wind Auction

- Standard Chartered Reiterates $94 Brent Call

- Chevron, Hess Confident Embattled Merger Will Close Mid-2024

- Analysts Flag 'Remarkable Feature' of 2024 Oil Price Rally